Published by Global Policy Journal, January 15, 2019

The next era of global economic expansion must better account for the inner tension between its levelling and gravitational forces. How can we grow our economies without growing hyper-concentrated wealth?

“In the early dawn, the city folded and collapsed. The skyscrapers bowed submissively like the humblest servants until their heads touched their feet; then they broke again, folded again, and twisted their necks and arms, stuffing them into the gaps.”

In Folding Beijing, an award winning novelette by the up-and-coming Chinese science-fiction author Hao Jingfang, Beijing is a massive machine rotating people in and out of the sunlight. How much sun one enjoys depends on economic class. One side of the Earth is the luxurious First Space where five million people enjoy a full day of sun. The other is home to fifty million people who enjoy less light and live harder lives.

Hao’s urban dystopia stands in a long tradition of science-fiction stories drawing attention to oppression and injustice. Ninety years ago, Fritz Lang’s silent movie Metropolis evoked a similar image. Metropolis is a city of skyscrapers where the wealthy live at the top; and down below, in subterranean factories, the proletariat leads a miserable existence, literally being devoured by the giant machine that powers the city.

Both stories are metaphors for an existential conflict between growth and inequality which lately gave birth to new political movements from the UK to the US to France, and radically revamped political landscapes. They cast the concentration of wealth in the hands of a few as an innate contradiction of market economies, and ask a big question: How can market economies expand without growing hyper-concentrated power and wealth?

For to all those who have, more will be given

The two science-fiction tales arrive at rather discomforting answers. Metropolis, written in between two devastating wars, is a sweeping story of rebellion without happy ending: when the workers smash the power generators, the water pumps fail, and their living quarters are flooded. Folding Beijing, written under the impression of China’s extraordinary yet uneven economic rise has a happy ending without rebellion. Lao Dao, the hero of the story, travels between the three sectors to convey a secret letter to earn some extra money to pay for his daughter’s school. Despite seeing the vast injustice, it is not upon him to question it. All he wants is to succeed in his mission.

Endure extreme inequality or fight it at the risk of total collapse. Both options are troubling and yet disturbingly plausible. For globalized economies to thrive, they must confront and keep confronting the explosive tension between two fundamental laws: one nurturing the equalizing effect of global markets, the other describing the tendency of unfettered markets to descend toward monopoly.

The first goes back to the economist Paul A. Samuelson. In 1948, he published an idea that would influence generations of policy-makers: the “factor-price equalization theorem”. Building on Adam Smith and nineteenth-century liberal economists it argues that, under conditions of unlimited trade, competition would equalize factor prices, including wages. In the new market equilibrium, people would not need to move abroad to earn more, and businesses could not move abroad to pay less.

Samuelson’s theorem describes the vast levelling effects of market expansion, the “First Law of Globalization”, popularized in the famous expression “the world is flat”.

“The world will be enriched… as they become consumers, producers, inventors, thinkers, dreamers, and doers,” the author and commentator Fareed Zakaria wrote in the spring of 2008. And many did: in 1988, a lower-middle-class US citizen earned more than six times the amount of a well-off middle-class citizen in China. Today, both earn the same. Similar leaps happened in other economies, from Turkey to Viet Nam.

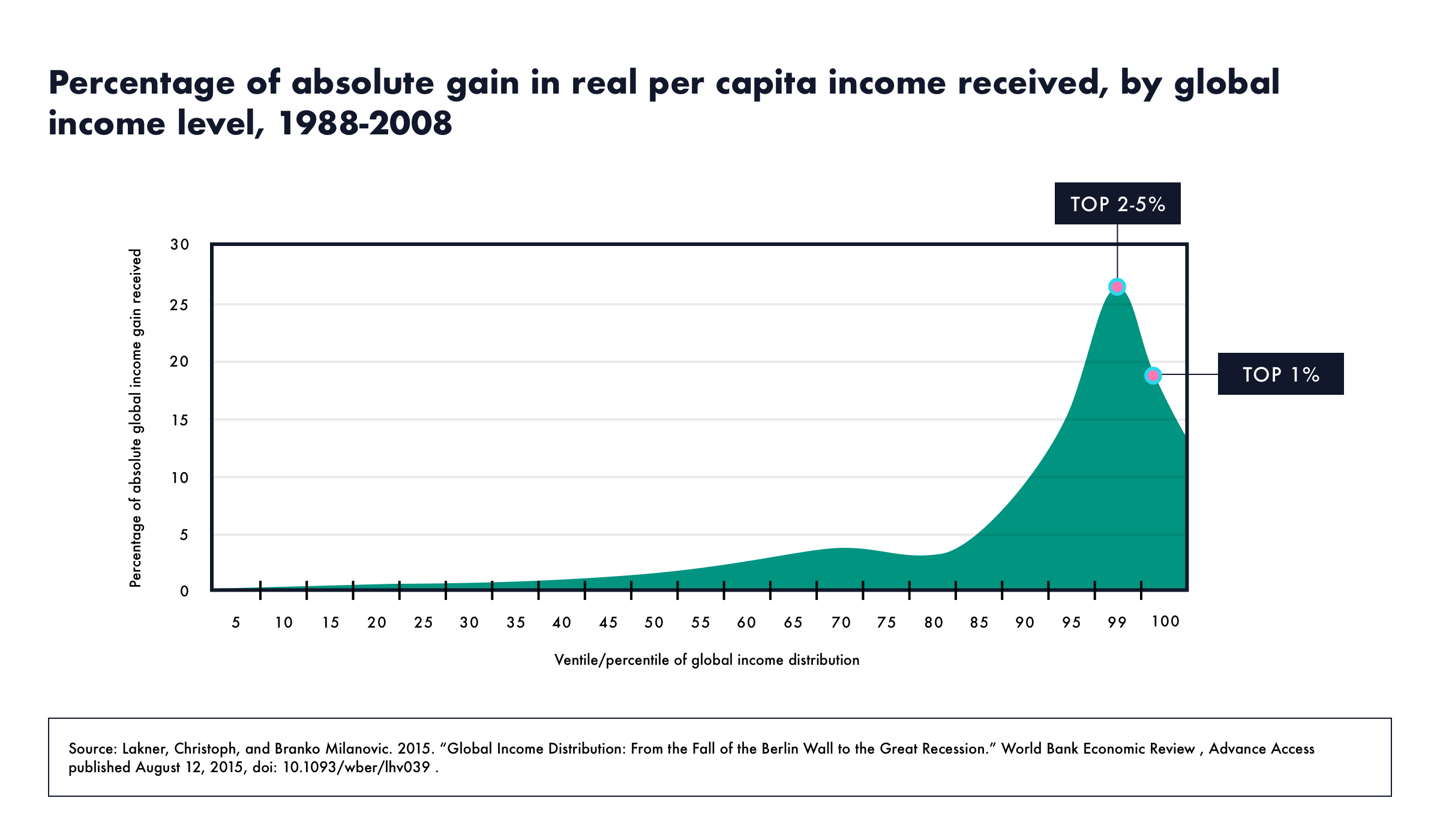

But when the financial crisis struck, cracks in that story began to grow wider. The financial collapse turned the public eye to the flipside of expansion: the concentration of everything, from people in cities to assets on balance sheets. From 1988 to 2008, about half the wealth the world amassed went to the wealthiest 5%, and almost one-fifth went to the top 1% of the population. As a consequence, inequality in rich and fast-growing developing countries went up – and stayed high; a phenomenon difficult to reconcile with Samuelson’s theorem and other expressions of economic orthodoxy.

Economists had ignored an aspect that sociologist Robert Merton in the late 1960s would call the “Matthew effect” after the biblical verse: “For to all those who have, more will be given, and they will have in abundance” (Matthew 25:29). It took until 1999 for physicists László Barabási and Réka Albert to find theoretical proof of this thought: networks, they posited, do not grow in egalitarian ways – new nodes prefer old ones that have many links; not because they must, but because it makes sense. The two scientists found what could be called the “Second Law of Globalization”, the law of concentration.

The fault line between supporters and critics of global markets often runs between those emphasizing Samuelson’s First versus Barabási’s Second Law. The globalization discourse is stuck because both sides fail to appreciate the intricate connection between the two laws, as in the famous optical illusions by M. C. Escher, where the observer sees squares pop out of a page or recede but cannot see both pictures at the same time.

Economic networks are neither liberating nor domineering, they exhibit at the same time an increase in diffusion and concentration.

Big cities, big sectors, big business

The expansion of the world economy resulted in an era where power and wealth are not only more concentrated, but also more dispersed than ever. Globalized markets connected hundreds of millions of citizens as consumers and producers and thus lifted millions out of poverty, but they also created huge rents for those exercising control over the central nodes of the network. The result is a global economy that is highly uneven across levels and scales, from geographic to sectoral to organizational.

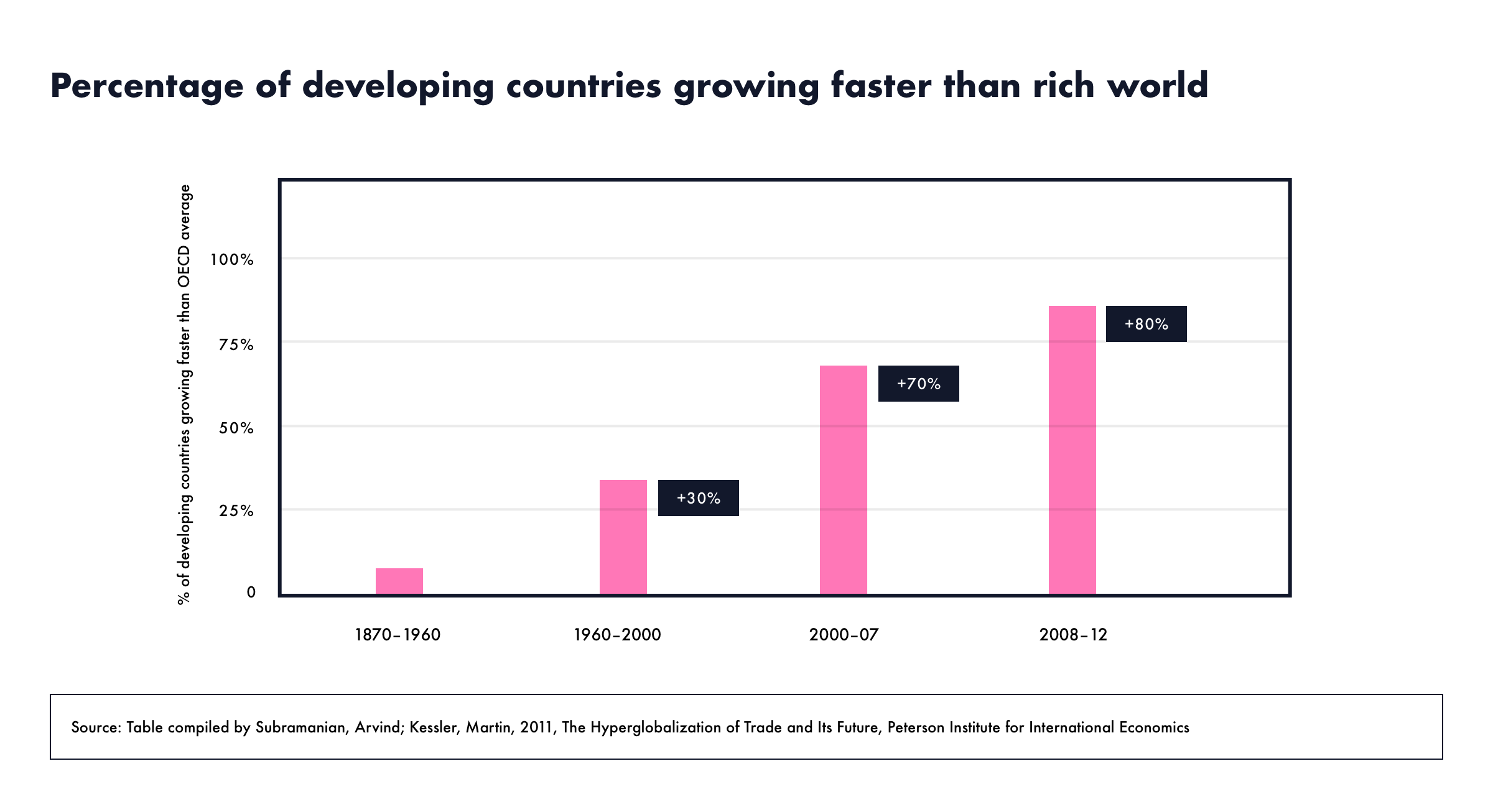

First, globalization drove apart the geography of growth: from the mid-19th century well into the 1960s, very few developing countries grew at a faster rate than Europe and the US. Between 1960 and 2000, about 30% grew faster; before the financial crisis this rate went up to more than 70%; today, eight out of 10 developing countries are growing faster than the OECD average. Since the early 90s, over 60% of growth has emanated from emerging markets. No wonder the geographic levelling of wealth was enormous.

But this is just one side of the story. The unparalleled expansion triggered an equally stark concentration. In the early 1800s, just 3% of the world’s population lived in cities. Today, it is over 50%. Large cities are gateways to the world, critical nodes in a global web of roads, routes, cables and pipes. In countries like Brazil, Turkey, Russia or Indonesia, the biggest city accounts for over one-third of total GDP. Big cities are hugely affected by the Matthew effect, feedback loops of capital, talent, innovation and growth. As Richard Florida put it in his latest book: “Cities are not just the places where the most ambitious and most talented people want to be – they are where such people feel they need to be.”

Second, globalizing markets drove apart industry sectors. Throughout the 1990s and early 2000s, international trade grew twice as fast as GDP. However, not just goods, capital and people crossed borders. The broadening and deepening of economic ties also prompted the cross-border transfer of knowledge, letting countries shift resources to higher productivity and higher salary sectors. Technological innovation, the economist Paul Romer famously wrote in 1990, is not exogenous; it is directed by markets. Globalization not only equalized factor costs, it also closed knowledge gaps.

Harvard’s Atlas of Economic Complexity is widely known for tracking and visualizing the knowledge equalization effect of global trade. Its baseline is a network representation of product categories traded around the world, from coffee to machinery. Ricardo Hausmann, the founder and head of the project, compares these with letters in a scrabble game: more letters mean more words and more sectors mean more opportunities to combine industrial capabilities into products. Time series data show how the diffusion of knowledge across borders let countries expand into new products, boosting their economic complexity and, hence, their future growth potential.

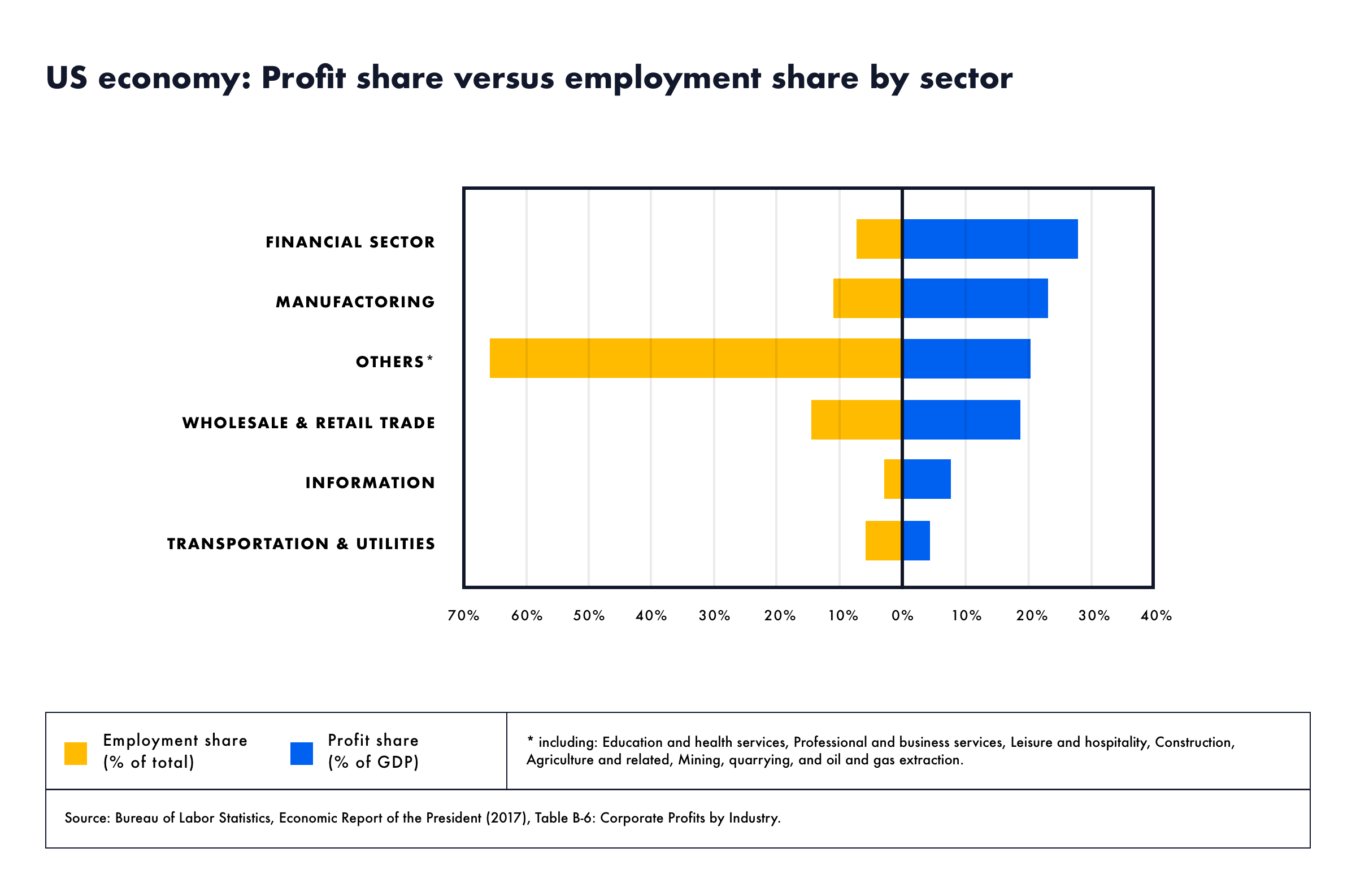

However, while economies became more complex, profits became more concentrated in a couple of key enabling sectors, most notably finance and information technology. The US financial sector only generates 4% of employment but generates over 25% of all corporate profits; moreover, an Economist survey found that about half the pool of abnormally high profits relative to GDP is going to tech firms.

More and more economists point out that the profits earned in these sectors reflect not an extraordinary capacity to create value, but rather an extraordinary capacity to usurp value created by others. In her book Saving Capitalism, Rana Foroohar stresses that, today, only 15% of capital from financial institutions is used for business investments. Similarly, digital pioneers like Jaron Lanier express concern about the lion’s share of the value generated on digital platforms flowing to those who aggregate and route it, and not to those who provide the “raw material”.

Lastly, the process of global expansion drove apart organizations. The number of Fortune 500 firms based in emerging markets has tripled since 1990 and could reach 50% by 2025, half of which will be based in China. Many emerging market businesses already belong to the world’s largest: firms like State Grid Corporation of China, China National Petroleum or Sinopec are matching not only big Western companies like Exxon or Apple, but also the GDP of large countries like Korea, Mexico or Sweden. Globalization levelled not only factor costs, but economic power, too.

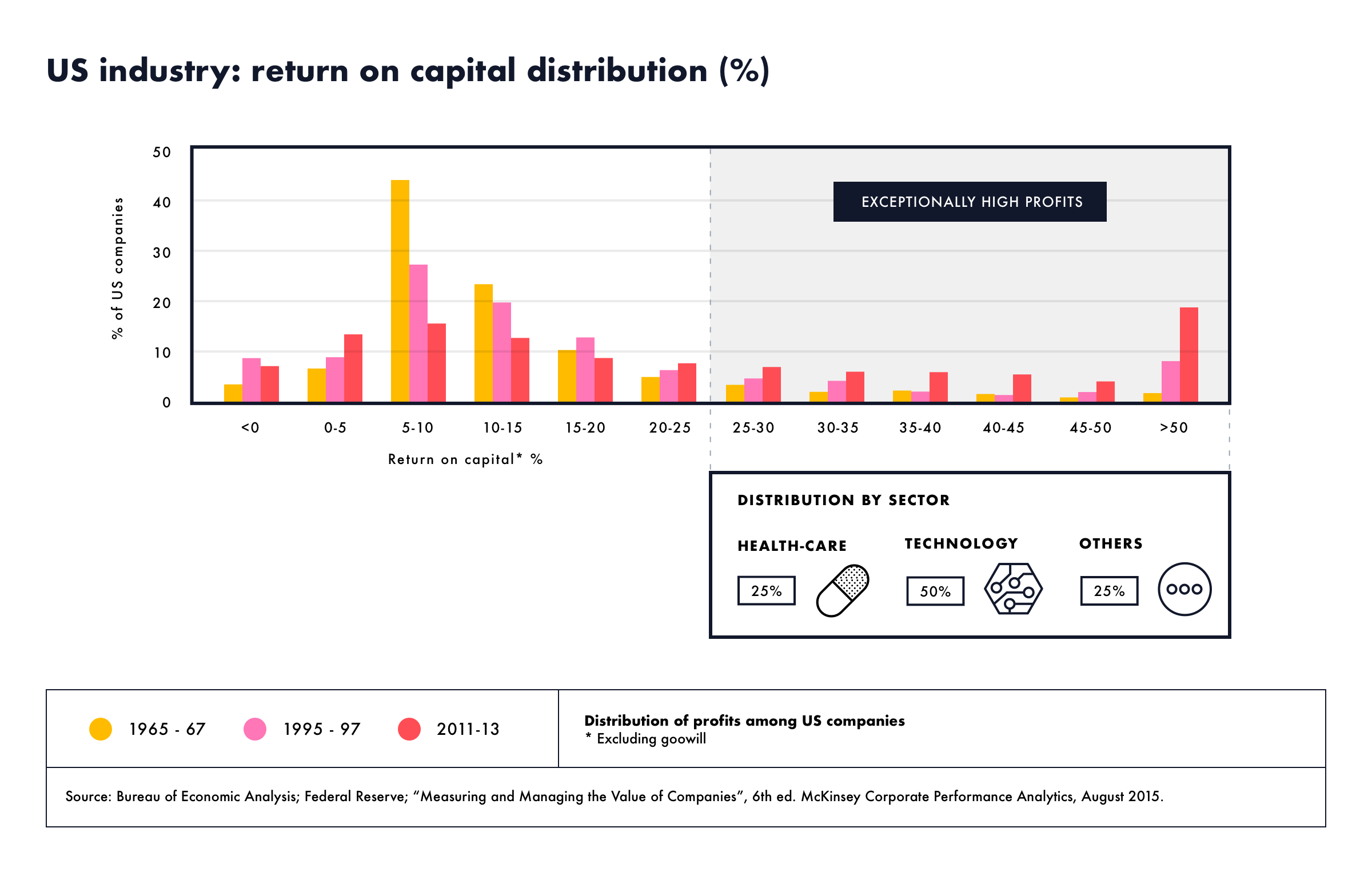

Yet, while headquarters of the top companies became more dispersed, profits became more concentrated. A study of US enterprises shows that, in 2013, the top 10% of businesses by profit were eight times more profitable than the medium ones, compared to three times in the 1990s. Joseph Schumpeter, one of the greatest economists of the 20th century, argued that one shouldn’t be worried by monopoly rents because fierce competition for the market would quickly erase the advantage. But corporate performance over the past decades draws a different picture: 80% of the firms that made a return of 25% or more in 2003 were still doing so ten years later. In the 1990s the odds were only at about 50%.

Some of this is related to internet giants, which benefit hugely from network effects. The other critical driver is acquisitions: a 2011 study analysed ownership structures of 43,000 transnational corporations, and found a “super-entity” of 147 tightly knit firms. Less than 1% of the network controlled 40% of all assets. Another study found that, in 900 sectors, two of three have become more concentrated since 1997. This created efficiency gains, but also weakened competition, allowing firms to hoard profits and invest less. American firms generate $800 billion a year in excess cash, or 4% of GDP.

The three concentration effects combined explain a large proportion of the rise in fragility and inequality. Most countries show significant wage gaps between urban and rural areas, and between small and large cities. The Santa Fe Institute calculated that those who move to a city twice as large are on average 15% better off. This is due to the compound effects of being connected to markets for goods, capital and talent, as well as a fierce competition for limited urban space that pushes out those with low incomes.

A study by Cesar Hidalgo reveals a similar kind of relationship between the concentration of economic activity in certain sectors of the economy and rising inequality: countries whose economies became less concentrated on a sector level, such as South Korea, saw reductions in income inequality, while those which became more concentrated, such as Norway, saw inequality increase.

On the level of organizations, the same trend is apparent. A study by Erling Bath, Alex Bryson, James Davis and Richard Freeman found that most of the growing dispersion in individual pay since the 1970s is associated with pay differences between companies and not within. The Stanford economists Nicholas Bloom and David Price confirmed this view in a study arguing that virtually the entire rise in income inequality is caused by a growing dispersion in average wages paid by firms.

When yesterday’s solutions become tomorrow’s problems

All that points to gravitational forces running against the levelling effects of globalization. This realization is not new. The observation that markets, left on their own, can produce gross imbalances is at the front and centre of Marxist political philosophy. The French economist Thomas Piketty gave new momentum to this argument in his tome, Capital in the Twenty-first Century, stating that “there is no natural, spontaneous process to prevent destabilizing, inegalitarian forces from prevailing.”

The benefit of studying economic expansion through the lens of networks theory, however, rests in how it reconciles seemingly conflicting schools of thought: concentration is not the opposite of dispersion but its inner tension. Global markets are the engine behind levelling the economic playing field and the main driver of inequality.

Treating concentration as inner tension of market growth sets it apart from the structural determinism of Marxism: as spot-on as Marx was in his perception of gravitational forces, as flawed were his prophecies of a predefined historical outcome, which later became a platform for totalitarian regimes to posit themselves as instruments of the “inevitable”.

If distribution and concentration are two sides of the same coin, the defeat of one is neither possible nor desirable. Rather than resolving the tension once and for all, the focus shifts to bending it to positive ends. We can’t ignore, let alone dissolve, this tension the way we can’t fly a plane by ignoring gravity. But we can hope to mobilize countervailing forces, the way engineers are lifting tons of metal and fibre into the sky.

In that regard, not Marx but his ancestor Georg Wilhelm Friedrich Hegel is a better choice for making sense of today’s mounting tensions between diffusion and concentration forces. A witness to the French Revolution, the philosopher concluded that our world is not finite and inconsistent because it is thwarted by external obstacles; it is thwarted because it is finite and inconsistent.

The enemy is the materialization of inborn tensions. The more our identity hinges upon us opposing it, the more likely victory will result in our own defeat. Such was Xi Jinping’s message to leaders in Davos in 2016: “Pursuing protectionism is like locking yourself in a dark room, which would seem to escape the wind and rain, but also block out the sunshine and air.” You don’t only lock out the enemy, you lock out yourself.

An enlightenment thinker, Hegel considered self-mastery and self-understanding as key to overcoming the inert inconsistencies of our solutions. We create the market to serve us, but before we know it, we end up serving the market. Does that make markets a bad idea? The answer according to Hegel lies neither in the thesis nor in the antithesis, but in a synthesis that reconciles the two. No idea is ever perfect, no solution final.

When a concept begins to impede our progress, it needs to be transcended. To Hegel, there was no law of history that pre-exists the contingent process of its actualization. The only necessity is to confront our inconsistencies, to challenge past solutions when they become tomorrow’s problems – to master gravity, not to succumb to it.

Globalization must engage with its inconsistencies

What would Hegel have made of the new struggle between globalists and protectionists? He presumably would not have simply taken sides but insisted on the mediation of the opposites. Markets paved the way to modernity by challenging old aristocratic elites, but also gave rise to new industrialist ones. Under great struggle, varieties of social capitalism emerged to resolve this tension by asserting more rights to the workers.

The neoliberal project dating from the late 1970s identified Big Government as the central impediment to prosperity. Facing growing competition from abroad, the pendulum swung from concerns over firms converting their profits into political influence and corroding the market and the machinations of government, to concerns over government protecting bad companies in the name of competition, and to the detriment of consumers and employees. In the Reagan and Thatcher era, market capitalism became more favourable to vertical and horizontal mergers, and the policy focus shifted from principally protecting competition to principally protecting consumers.

These shifts played a major role in jump-starting the hyper-globalization age, but also laid the ground for the 2008 crisis and the rise of extreme inequality. Slowly, a new consensus is forming among economists that competition has weakened as a result of concentration and that the pendulum has swung too far in favour of incumbent firms. With US business spending $3bn a year on lobbying, economists fear it could abuse monopoly positions, or actively stifle competition. Each reform sought to battle the gravitational forces of its time, yet ultimately unleashed new ones on all levels.

This does not mean anything changes. The world is healthier, wealthier and safer than it has ever been. The Hegelian insight is that everything, without exception, requires energy just to maintain itself, let alone achieve improvement. To avoid the journey of decay from scale to fail, globalization must engage with its inconsistencies. Without that, globalization risks reactions similar to an autoimmune disease, where vital body functions are misread as an outside threat, igniting a sequence of self-destruction, like the rage against the machines in Metropolis. Even if inequality becomes unsustainable, it will not just go away; without systems to mediate the opposites, it will trigger dangerous dynamics that could destroy much else, including many lives and much wealth.

The defining challenge leaders face is to design healthier forms of economic expansion that don’t gravitate rapidly and unchecked towards extreme inequality. Rather than heating up old debates, we need a better question: How can we unlock the power of networks without unleashing the mercurial force of concentration?

Technology fuels distribution and concentration in equal measure

Technology will play a decisive role in shaping the answer. But it won’t decide. The Fourth Industrial Revolution, a new era where digital technologies perfuse physical and biological spheres in unprecedented ways, will supercharge forces of diffusion and concentration in equal measure. It could benefit few exponential enterprises or millions of connected mini-multinationals. It could concentrate wealth in the hands of those who control nodes in the network or turn these nodes into platforms that distribute value more fairly. It could suck more people into megacities and deepen the rift between urban and rural areas or it could enable smart spatial designs that transform large cities into compact connected units that transcend the old urban-rural divide.

The challenge is that both futures are linked. The e-commerce giant Alibaba, for instance, launched a massive effort to connect China’s rural areas to its market place. In over 1000 rural Chinese communities over 10% of the population are now making a living by selling products from electronics to children’s toys on Alibaba’s trading platform Taobao. “Taobao villages” have come to play a major role in the country’s goal to eliminate absolute poverty by 2020. Alibaba helps realize the vision of an economy run by lots of mini-multinationals – whilst expanding its market power.

Policy-responses to mounting concentration need to recognize this tension. The stubborn persistence of profits over and above levels justified by investment or expertise requires smarter antitrust laws that not only focus on market share or pricing power but on many forms of rent extraction, from copyright and patent laws that allow incumbents to cash in on old discoveries to the misuse of network centrality.

The question is not “how big is too big” but how to differentiate between ‘good’ bigness and ‘bad’ bigness. The answer hinges upon the balance business strikes between value creation and value capture. As Tim O’Reilly wrote in a blog, “as networks reach monopoly or near-monopoly status, they must wrestle with the issue of how to create more value than they capture — how much value to take out… versus how much they must leave for others in order for the marketplace to continue to thrive”.

Secondly, economies need to make it easier for start-ups to scale. Many politicians pay lip service to the importance of entrepreneurship but especially in the US the number of start-ups has receded for some time. This is alarming because innovation and entrepreneurship remain the most effective antidotes to rent-extraction. From land-rights to cash transfers, digital ledger technologies curb the power of large oligopolies more effectively than heavy-handed policy interventions.

Capitalism needs churn but cannot just rely on the market to bring it about. Andrew Grove, the former Intel executive, wrote in a much debated essay that American start-ups struggle to scale because of the short-termism of financial markets and an eroding manufacturing base – both are immediate consequences of concentration on organizational and sectoral scales, triggered by the process of globalization.

Lastly, recognizing concentration forces should start a new debate about market societies. The common neoliberal rhetoric that “those who work hard and play by the rules should be able to rise” draws on a deep belief in the equalizing force of the market. The flipside of this idea, however, is what Michael Sandel calls “meritocratic hubris”, the misguided idea that success (and failure) is always our making.

For policy-makers this means that investments into education and skills are necessary but not sufficient to address the inequality problem. They must be met by measures that tackle structural biases head on, from minimum wages to, potentially, a basic income.

For connected economies to continue to thrive, they must tackle the gravitational forces in their organizations, sectors and geographies. Globalization needs a middle since otherwise there is no market. However, a strong middle, a bell-curve income distribution of sorts, is never a self-enforcing equilibrium. It must be maintained as much as an airplane needs thrust to hold its height.

With new trade wars waged, economic globalization hits a breaking point. Old categories of left and right are losing their meaning, whilst new fault lines emerge between those who seek to smash concentration by smashing globalization, and those who seek new forms of expansion that don’t gravitate into extreme inequality.

Whilst both movements seek to disrupt the old structures, one is about dismantling global economic integration with both its risks and opportunities for development and progress. The other is about building a better architecture with strong pillars and smart passageways that withstand the corrosive effects of concentration.

Illustration by Oliver Barrett